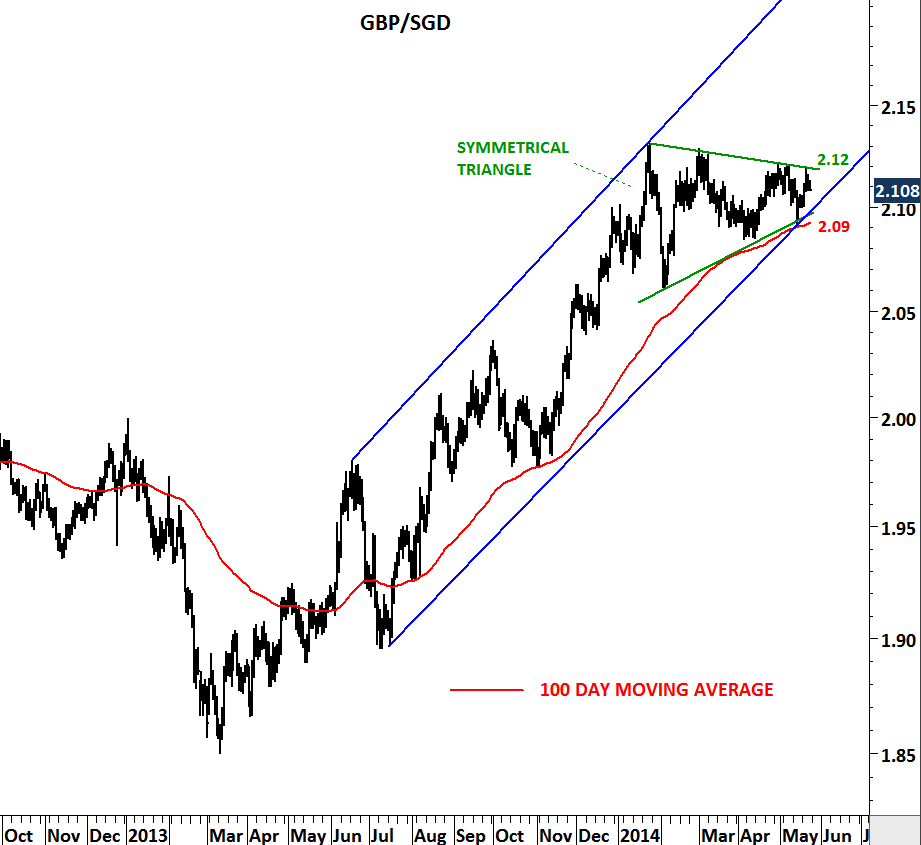

GBP/SGD

Long-term trends can be interrupted by short/medium-term consolidations; in other words “breath-taking” periods. In technical analysis these type of short/medium-term consolidations are classified as flag, pennant, triangle or rectangle chart pattern. Each chart pattern has its own characteristics.

Since the beginning of 2013, British pound has been outperforming Singapore dollar. Cross rate formed a clear uptrend. After reaching 2.13 levels in the beginning of 2014, GBP/SGD started moving sideways to form a common consolidation pattern known as symmetrical triangle. Volatility on daily and weekly scale suggests another trend period is likely to unfold following the latest consolidation. Breakout above 2.12 levels will be bullish for British pound and GBP/SGD cross-rate will target 2.15-2.18 area. As long as the cross rate remains above 2.09 levels the uptrend will remain intact.