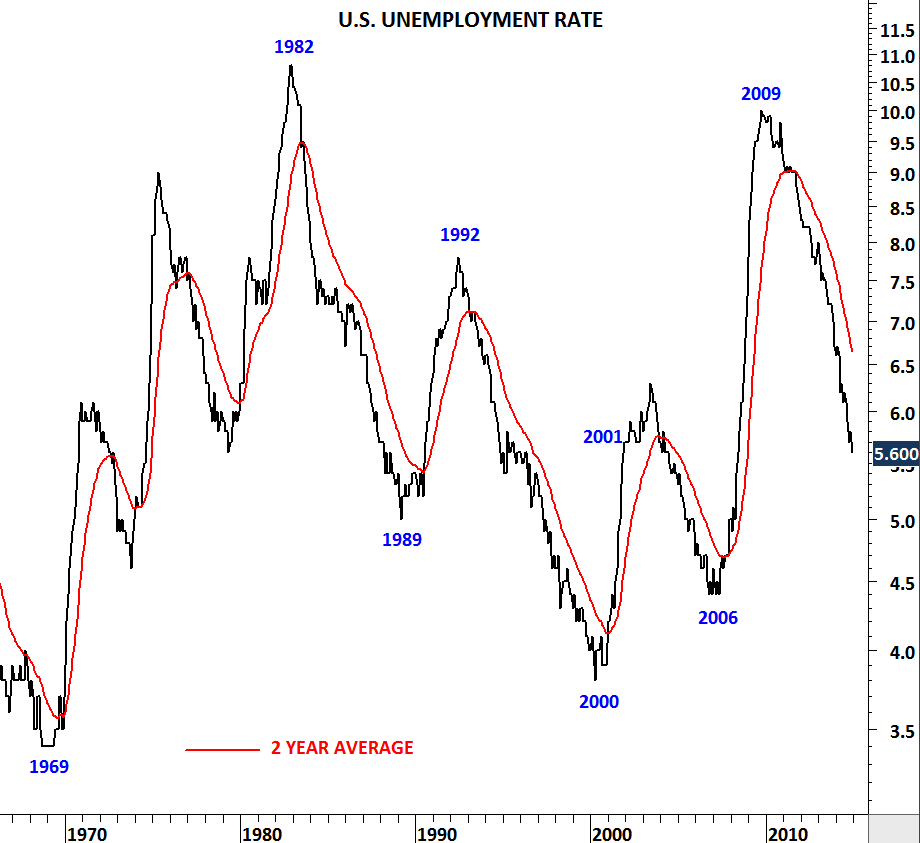

U.S. UNEMPLOYMENT RATE

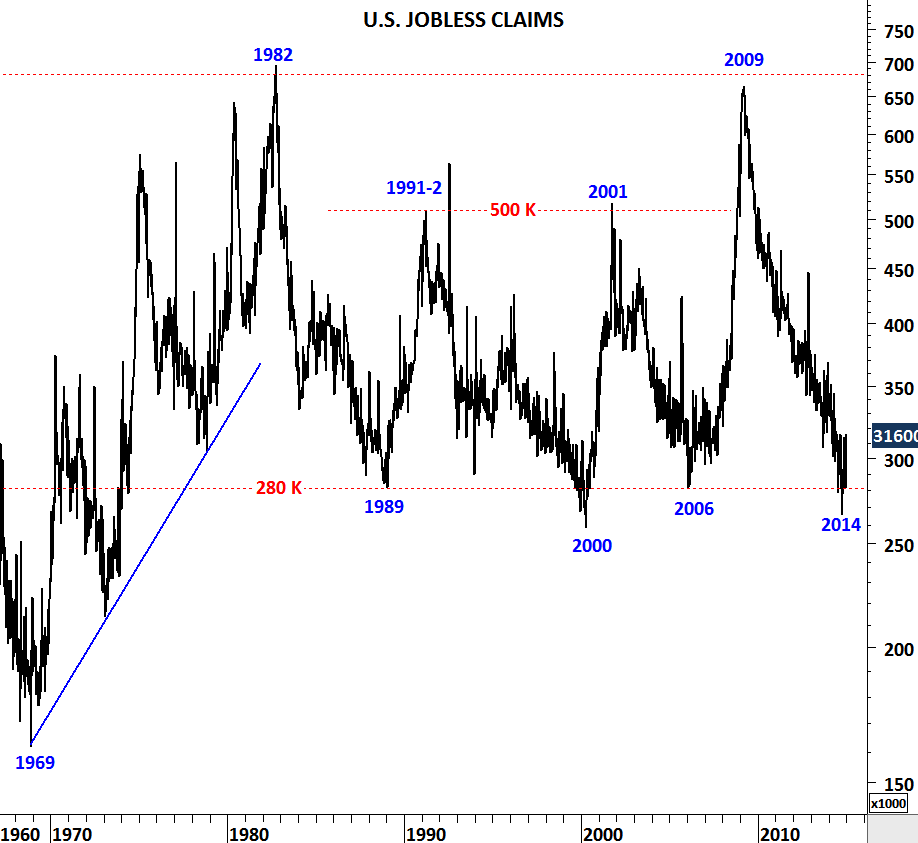

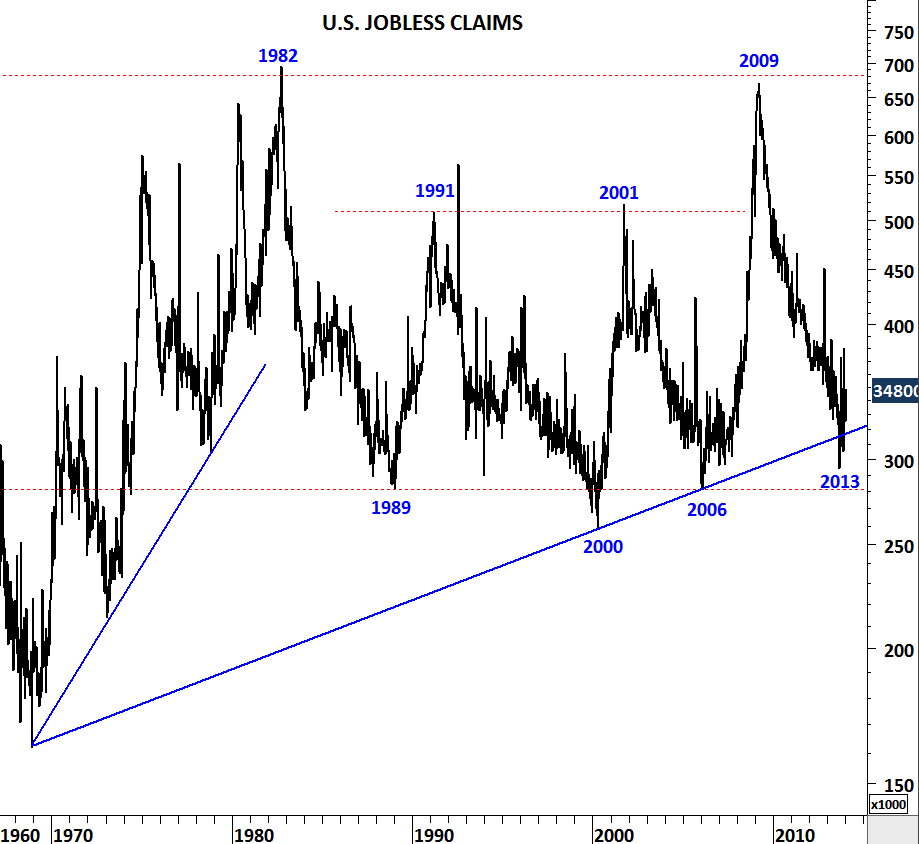

Two-decade long horizontal support at 280K on the U.S. weekly jobless claims chart suggest we might be at a “positive extreme” for the U.S. job market. 1989, 2000 and 2006 have proved to be the lowest levels for the weekly jobless claims. Reversals from 280K area resulted in a weak U.S. job market in the following years. Unemployment rate moved higher following the years 1989, 2000 and 2006. In 2014, U.S. weekly jobless claims reached as low as 266K. Latest data stand at 316K. Every long-term trend has an end. Historical levels on the long-term charts are warning us of a possible reversal. It is important to keep an eye on these two long-term charts in the following months.