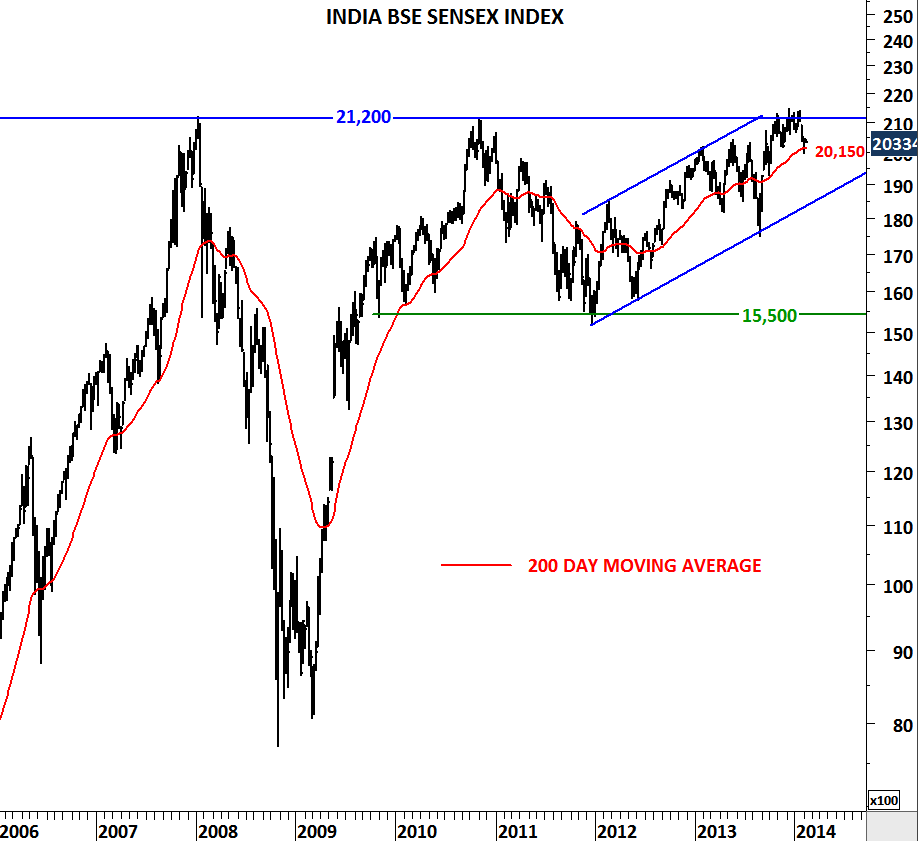

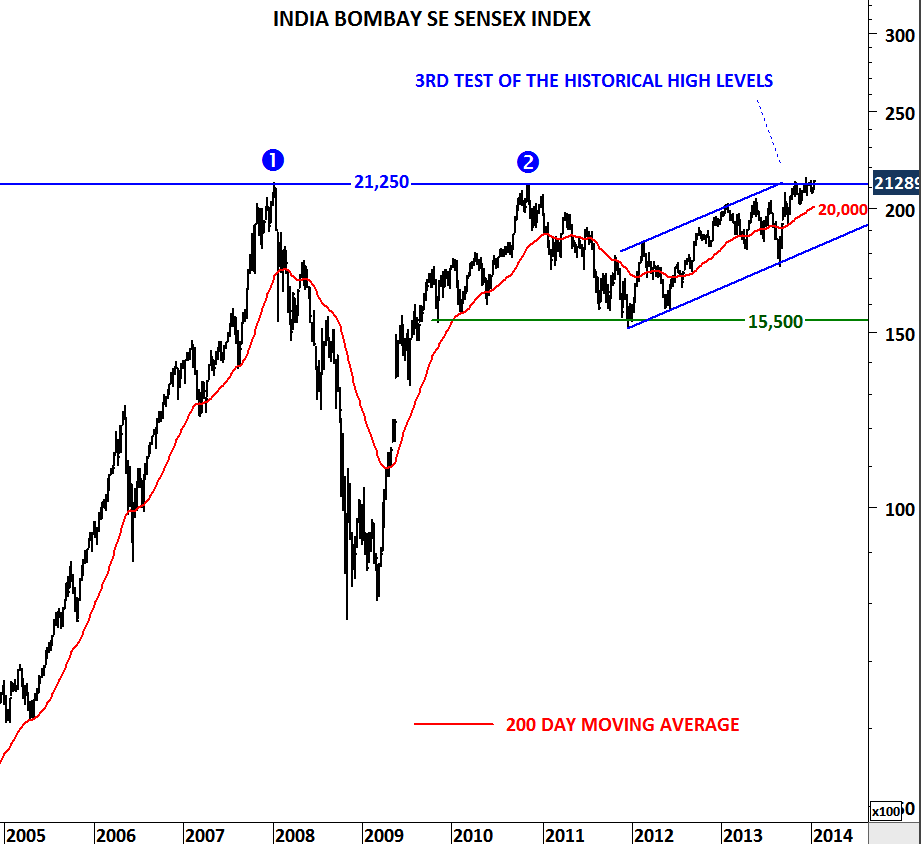

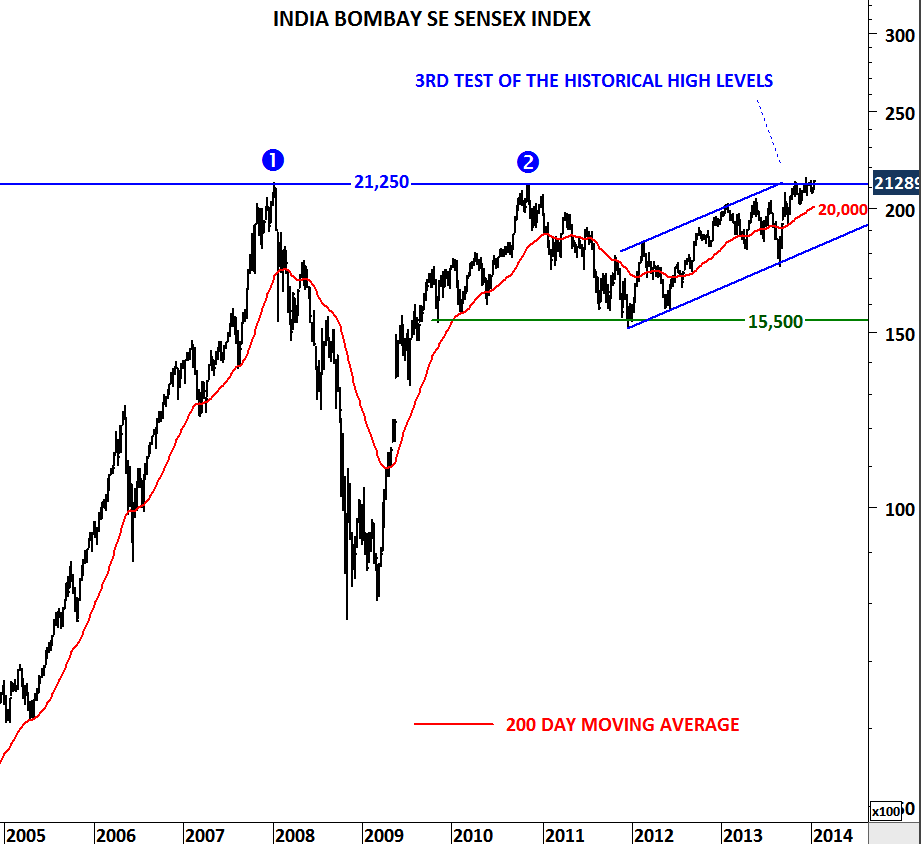

INDIA BSE SENSEX

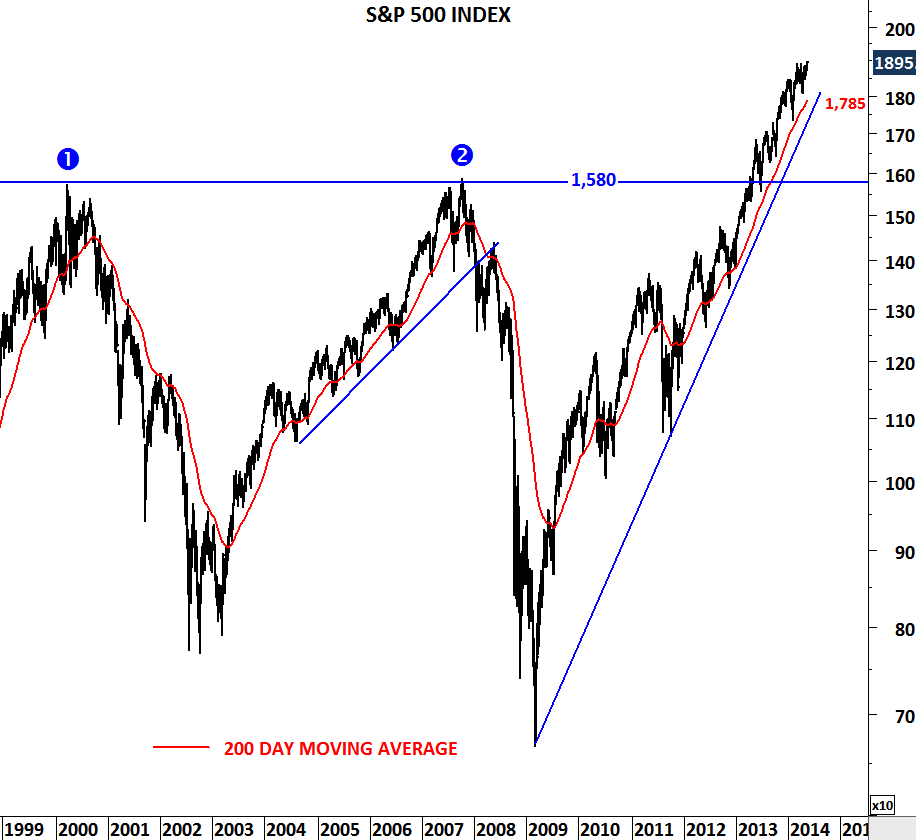

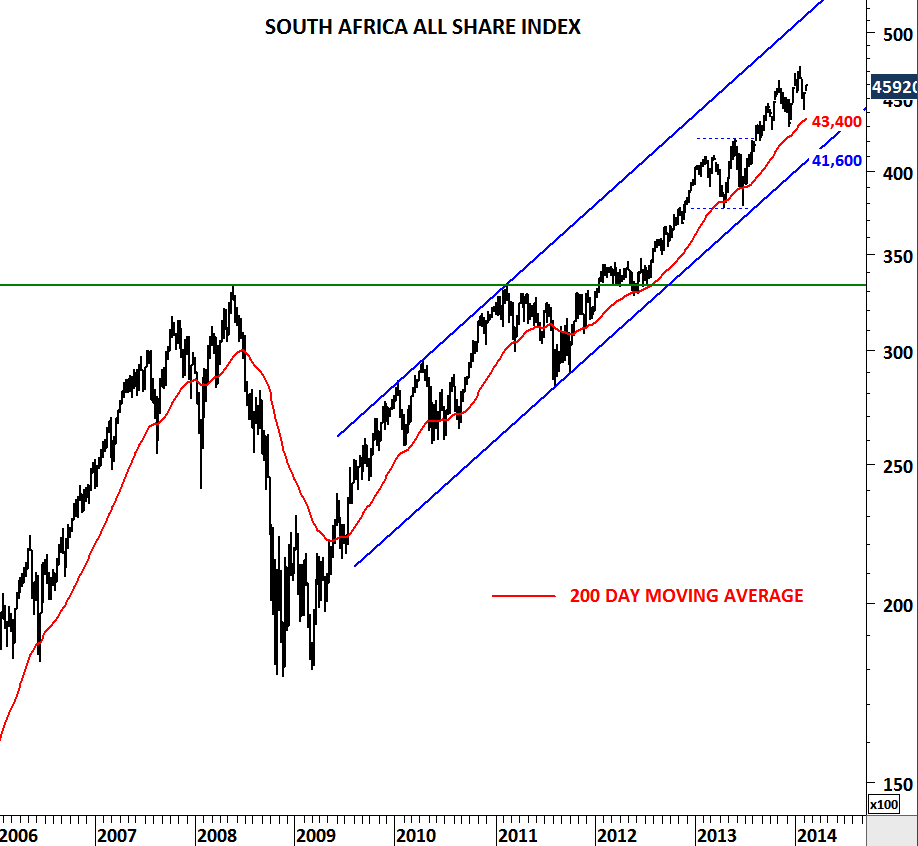

Markets that breakout to all time high levels usually don’t look back. Price enters the uncharted territory where it doesn’t meet any resistance. Some breakouts fail and fall back below the resistance they breached earlier. At that point we know that something was wrong with the earlier breakout. However most of the breakouts to all time high levels are so powerful and decisive that they don’t leave the price action in question. India’s breakout has been one of those set-ups where breakout to historical high levels from low volatility period is now being followed by a strong upward trend. This is extremely positive for Indian equities and suggests higher prices in the medium-term. I attached below similar breakouts to all time high levels on South Africa All Share index and S&P 500 index. (For earlier analysis on India you can refer here)